Back when the virus that would soon be known as Covid-19 was just a blip on the radar, Selco wrote an article called, It’s Not the Virus You Need to Worry About. It’s the System. And like much of what Selco writes, it was prophetic.

Here we are, coming up on a year after the virus first began making itself apparent and the world is dramatically different. Not only are there the inevitable arguments about masks, lockdowns, vaccines, and hypocritical politicians using the whole thing as a power grab, but there are very real effects on everyday families all over the world.

In the United States, our personal finances have taken blow after blow. Eight million more Americans than last year are now living in poverty as millions of jobs have disappeared, never to return. Data from the review site Yelp shows that 60% of the businesses that shut down due to Covid have permanently closed. People who were formerly struggling are sinking, and many of those who were comfortably middle class are desperately trying to stay afloat.

- Buy All-American!

- Bring health and vitality back to your body with these non-transdermal patches

- Get your Vitamin B17 & Get 10% Off With Promo Code TIM

- How To Protect Yourself From 5G, EMF & RF Radiation - Use promo code TIM to save $$$

- The Very Best All-American Made Supplements On The Market

- Grab This Bucket Of Heirloom Seeds & Save with Promo Code TIM

- Here’s A Way You Can Stockpile Food For The Future

- Stockpile Your Ammo & Save $15 On Your First Order

- Preparing Also Means Detoxifying – Here’s One Simple Way To Detoxify

- The Very Best Chlorine Dioxide

- All-American, US Prime, High Choice Grass-Fed Beef with NO mRNA, hormones or antibiotics... ever!

It isn’t so much the virus that has caused our financial woes – it’s the response to the virus. Federal, state, and local governments have deemed what businesses are allowed to operate and how they must do so. This has resulted in the loss of businesses themselves, loss of sales, and loss of jobs. Nearly every family is feeling the effects to some degree. Please check out our new frugality website for practical solutions if you are dealing with financial issues.

Here are some of the ways American families are suffering financially due to the response to the virus.

More people are living paycheck to paycheck.

Back in February of this year, a report was released that showed 40% of American workers were living paycheck to paycheck.

Willis Towers Watson’s Global Benefits Attitudes Survey discovered that although 58 percent of workers think their finances are heading in the right direction, 38 percent of employees are living paycheck to paycheck…

…Almost one-fifth of those making more than $100,000 are living paycheck to paycheck, and about one-third say their financial problems negatively affect their lives. The survey polled 8,000 American workers. (source)

That early 2020, pre-lockdown report looks like a glimpse of nostalgia from the good old days. A more recent report has found, due to the Covid response, that now almost two-thirds of Americans are living the paycheck to paycheck life.

With government shutdowns forcing countless businesses to close and then lay off workers, one in four respondents now feel their income is not stable. Nearly two in three (63%) say they’re going paycheck-to-paycheck since March 2020. Millennials seem to be the hardest hit, with 64 percent saying they’re living off their paychecks.

“After the unemployment rate spiked to more than 14% in April, Americans continue to be wary about their job security and income,” writes Highland President Jon Berbaum in a media release. (source)

Anyone who has ever lived through this situation knows that paycheck-to-paycheck is a delicate dance and it only takes one small thing to go wrong to cause your house of cards to come tumbling down.

NSF fees, late fees, reconnection fees, extra deposits, overdraft interest, and payday loans can all destroy the financially fragile, leaving them in a downward spiral designed to keep them trapped. There’s a reason that broke people tend to stay broke, and it’s not because they’re simply lazy and irresponsible. It’s because the system is set up in a way that it earns more money by charging poor people extra.

Hardly anyone has an emergency fund left.

Back in 2019, Bankrate released a survey that said only 40% of Americans would be able to pay for an emergency costing a thousand dollars out of their savings. Yet again, those were the good old days.

A more recent survey said that an astounding EIGHTY TWO PERCENT of Americans could no longer handle an emergency costing $500. Zero Hedge reports:

But perhaps the most alarming number from the entire survey: a whopping 82% of respondents said they wouldn’t be able to cover an emergency $500 expense without borrowing money.

For context, prior to the pandemic, surveys showed that roughly half of Americans couldn’t afford a $500 emergency expense, which means the number of people who say they couldn’t cover a small emergency has risen by 60%. (source)

An emergency fund is the most important financial prep you can make.

When your finances are tight, sometimes your first impulse is to spend every dime. Many people focus on things like paying off debts, stocking up on food and supplies, or paying more than the minimum payments on bills.

However, that may not be your best bet. Don’t get me wrong – paying off debt is absolutely vital, but most experts recommend establishing an emergency fund as the first step back to financial security. (source)

Many people report making up the difference between their income and output with credit cards and other forms of personal debt. Unfortunately, with our somber economic forecast, this is just delaying the inevitable implosion of their personal finances.

People are unable to find work.

An October jobs report showed that millions of the positions lost back in March have not returned, and that millions of people have now reached the classification of “long-term unemployment.” The New York Times reported:

The Labor Department said on Friday that 2.4 million people had been out of work for 27 weeks or more, the threshold it uses to define long-term joblessness. An even bigger surge is on the way: Nearly five million people are approaching long-term joblessness over the next two months. The same report showed that even as temporary layoffs were on the decline, permanent job losses were rising sharply.

Those two problems — rising long-term unemployment and permanent job losses — are separate but intertwined and, together, could foreshadow a period of prolonged economic damage and financial pain for American families.

Companies that are limping along below capacity this far into the crisis may be increasingly unlikely to ever recall their employees. History also suggests the longer that people are out of work, the harder it is for them to get back into a job. (source)

In September and October, many large corporations made the decision to end even more jobs.

Disney announced this past week that it would lay off 28,000 U.S. employees as its theme parks struggle. Layoff notices filed with state authorities show that hospitality and service companies across the country, from P.F. Chang’s restaurant branches to Gap stores, are making thousands of long-term staff reductions. Airport bookstores in Pennsylvania and Tennessee are cutting jobs as travel dwindles. So are wineries and upscale sports clubs in California.

Airline job cuts run to the tens of thousands. American Airlines started to send furlough notices to 19,000 workers and United Airlines to 13,000 after a federal moratorium expired on Thursday. Those are on top of reductions at other carriers, and existing firings across the industry.

Altogether, nearly 3.8 million people had lost their jobs permanently in September, according to the Labor Department’s latest monthly survey, almost twice as many as at the height of the pandemic job losses, in April. (source)

The closure of schools has kept many parents from returning to work or caused financial hardship.

It isn’t just the unavailability of jobs that has made things difficult. The erratic 2020 school year has also caused financial hardship and in many cases, made it impossible for parents to return to work.

Now, I know a lot of homeschool parents will say that people shouldn’t be using public school as a free babysitter. But the fact remains that many families require two incomes to survive. In my case, as a single mom, the school year allowed me to make a living. During the summer, my children had wonderful vacations with both sets of grandparents, mercifully, because paying for full-time childcare for both of them would have taken almost every dime I was earning, leaving nothing for housing, food, and other costs.

If you aren’t familiar with current childcare costs, a person quoted in the article cited below reported that she and her husband were spending an eye-watering $5300 per month for their three children.

While wealthier parents can afford to “get creative,” lower income and many single parents have far fewer options, said Caitlyn Collins, a professor of sociology at Washington University in St. Louis who studies women and families. Some are leaning on family members or just doing the best they can on their own. Others have been laid off, or have had to quit their jobs to take care of their kids…

…The United States has been an outlier on child care long before the coronavirus, Collins said, with price tags far exceeding those in other high-income countries. The average cost of child care for a child under 4 is $9,589 per year, according to New America’s Care Report — more than the average cost of in-state college tuition. It’s much more expensive in big cities: In Washington, D.C., the average cost of care for an infant is more than $24,000.

Rising child care costs are particularly “terrifying” for U.S. families, Collins said, because child care already accounts for an enormous part of their budget, often second only to a family’s rent or mortgage. (source)

Financially speaking, women are suffering the most with regard to pandemic related job losses. Hundreds of thousands of women left the workforce in September – approximately 849,000 – in comparison to 216,000 men. Betsey Stevenson, a professor of public policy and economics at the University of Michigan, explained in an interview why women have been unevenly affected.

…the age group that had the biggest decline was thirty-five to forty-four. And it’s not at all surprising to me, in the sense that the people who are really struggling are people with young kids and multiple kids at home. It’s the parents who have a four-year-old, a six-year-old, and a nine-year-old, and those kids are at home, and they’re trying to do Zoom school. It’s really difficult. Even if both parents had the opportunity to work from home, that’s a really hard thing to manage. I want to make sure that I emphasize that that’s one kind of hardship, and then there’s another kind of hardship, which is parents or single moms who had an in-person job and no child care. (source)

I have more than one friend who has been attempting to oversee “distance learning” while keeping her job remotely and the stress levels are through the roof. If you can’t afford a nanny or you don’t have a family member willing to take on the task, quite simply, someone is going to have to stop working at a time when we can least afford to have our incomes drop any further.

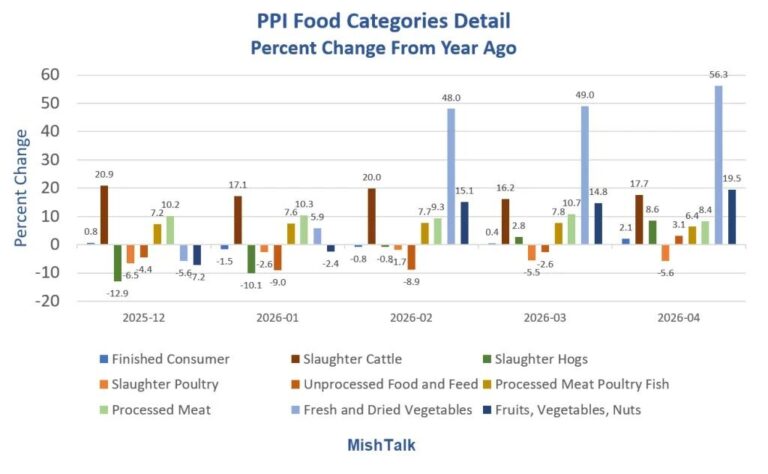

The price of food has increased dramatically.

Food prices increased for the fifth month in a row, according to the United Nations Food and Agriculture Organization. People around the world are seeing a 6.5% increase in their costs of commodities such as cereals, dairy, vegetable oil, meat, and sugar.

But your trip to the local grocery store may look like a much greater increase than six and a half percent. There’s a variety of reasons that prices have gone up. Everything from supply chain shortages to production issues has caused costs to increase. There are other Covid-related reasons that explain why you may be experiencing sticker shock:

Shift to eating at home: In a matter of two months, approximately $23 billion in consumer spending away from home was redirected toward grocery stores as restaurants were forced to close due to COVID-19, according to FMI – The Food Industry Association.

Loss of foodservice demand: When restaurants closed, farmers and ranchers lost a key channel for their product. With fewer buyers, it is costly or impractical to harvest, preserve or store some food and beverage products.Increasing production and processing costs: During COVID-19, companies have made investments and adjustments to safeguard their products and employees. This means costs for food production are higher. Some manufacturers have been able to innovate and find new markets for their products, but these changes often entail added costs.

Increasing operating costs for grocery stores: Compared to 2019, supermarket operating costs were up 7.9% in April 2020 and 6.7% in May 2020, according to USDA Economic Research Service.

Grocery stores have remained open during the pandemic and have had to quickly adjust to new regulations, safety and sanitation practices and enhanced customer education – all requiring resources. In addition, some areas of the grocery store, including salad bars and hot bars, have had to shut down, meaning a loss of revenue. (source)

There are also fewer sales:

Usually, 31.4% of grocery store items are purchased on some sort of sale, but at the end of September the share was 26%, according to market research firm Nielsen. The biggest impact was in the household care department, where just 15% of items were sold on promotion, half the usual amount. Heightened consumer demand and strained supply are giving stores little reason to mark down prices, Nielsen said. (source)

While the statistics only note a few percentage points, the real picture looks a lot different.

Eva Rosol was stunned during the summer when a rotisserie chicken that she could normally find on sale for $6 suddenly set her back $15…

….Ariel Neal, owner of Leira Knows Cocktails and Events, has been opting for more potatoes and starches and fewer fruits and vegetables…She didn’t qualify for unemployment benefits or small business relief, and has been subsisting on her savings and the government’s Supplemental Nutrition Assistance Program, formerly known as food stamps.

“Before, $20 would have gotten me at least two to three meals,” said Neal, 42, who lives in Calumet City. “Twenty dollars doesn’t do that anymore.”

…Yvernia Wilson, who is on a fixed income and vigilant about grocery prices, was taken aback early in the summer when a large package of hamburger meat she’d normally pay $8.99 for was listed at $14 at the Jewel-Osco she shops at on Chicago’s South Side.

A nice-sized pot roast for Sunday dinner was almost $20, $6 more than she’d usually spend. Even a package of chicken wings cost $3 more…

…Wilson restricts herself to two meats and for some items has resorted to buying cheaper brands she doesn’t necessarily like. She bypasses the organic aisle and sometimes forgoes fruit altogether if it isn’t on sale. (source)

Don’t look for food prices to decrease any time soon. Our supply chain is still broken and getting worse. Another lockdown means that store owners will be trying to get the most money possible from customers in order to keep afloat for as long as possible. The current price increases could be permanent.

The eviction moratorium runs out soon.

And finally, to make matters even more difficult for struggling families, a federal moratorium on evictions will be running out on December 31, leaving as many as 19 million people at risk of being homeless as 2021 begins. A few states will continue eviction bans but most will follow the federal guidelines.

It’s important to note that people who were not paying rent based on the moratorium will now have to catch up immediately or risk being evicted.

The federal mandate doesn’t prohibit late fees (although ), nor does it let tenants off the hook for any back rent they owe. It also doesn’t establish any kind of financial assistance fund to help renters get caught up, a safeguard some say is critical to preventing a massive wave of evictions when the ban eventually lifts…be aware that you may still be held responsible for any back rent you currently owe as well as any rent that accrues between now and the end of your lease (if you have one), whether or not you vacate. (source)

It’s projected that 6.7 million households could be affected by the end of the moratorium.

This is, of course, a double-edged sword. Not all rental property owners are massive corporate entities with teams of lawyers diligently searching for loopholes. This has been a tremendous hit for Mom and Pop landlords, many of whom invested in real estate to have a bit of income during their retirement. They have been unable to evict tenants who aren’t paying their rent but still had to maintain the property in a manner according to the local bylaws, pay their mortgage payments, and make timely property tax payments.

2021 isn’t going to be a magical solution.

A lot of folks have just written off 2020 as “a bad year” and seem to believe that the moment this year is over, the curse will be lifted and we’ll all be able to go on with our lives having survived it and gotten through it.

Unfortunately, the changes that I’ve written about aren’t going to disappear when you put that new calendar on the wall. Businesses that hung on through Christmas to try and sell their remaining inventory could be closing right after the holiday, leaving even more jobs in the dust. Lockdowns could very well become even more stringent after the inauguration, which would keep all the same problems going. It’s time to redouble your preparedness efforts and really examine your situation.

This has been more than a pandemic. It’s been a major economic catastrophe, just as predicted, and we’re in it for the long haul.

Article posted with permission from Daisy Luther

{kind=link}