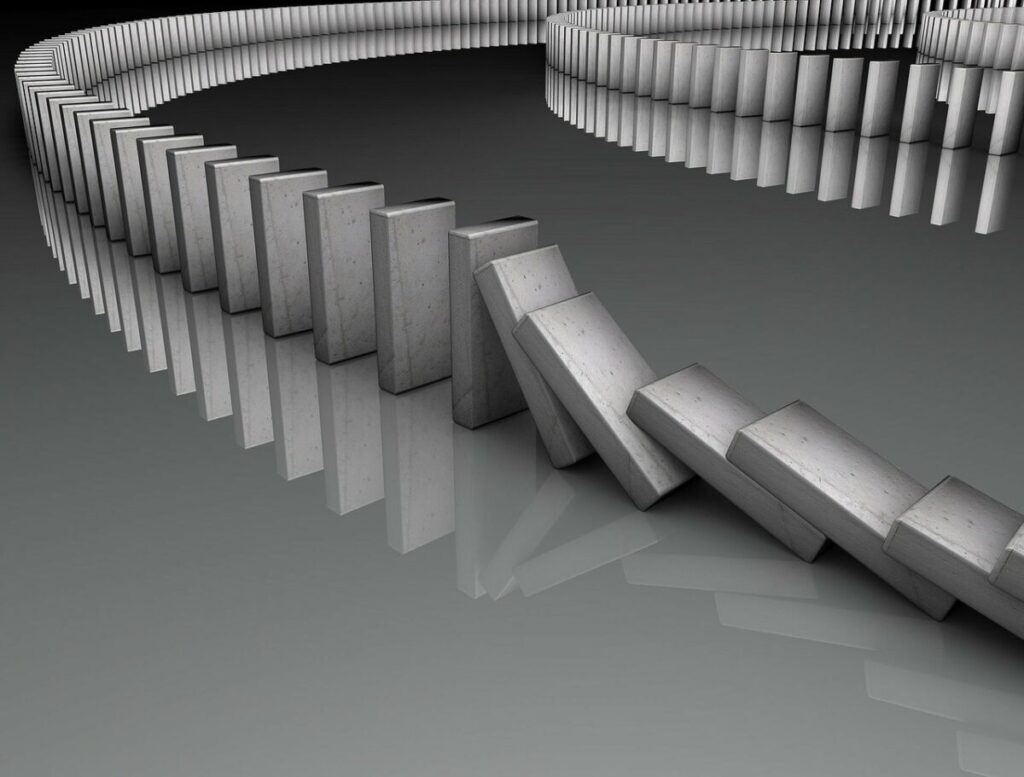

Welcome to the great banking collapse of 2023. Please try to enjoy the ride. When FTX crumbled, I explained to my readers that it was not the first domino to fall and that it certainly would not be the last. Sadly, that prediction turned out to be completely accurate. Within the last week, we have witnessed the second and third largest bank collapses in the entire history of our country. But Silicon Valley Bank and Signature Bank are not unique cases. The Federal Reserve created a 620 billion dollar blackhole in our banking system by aggressively raising interest rates, and our quadrillion dollar derivatives pyramid scheme is starting to tremble violently. The Federal Reserve is desperately trying to fix things by recklessly spraying money around, but the truth is that Fed officials are ultimately going to need a much bigger hose.

The speed at which financial institutions can collapse in a digital economy is absolutely breathtaking. It is being reported that 42 billion dollars was withdrawn from Silicon Valley Bank in one day alone…

Customers withdrew $42 billion in a single day last week from Silicon Valley Bank, leaving the bank with $1 billion in negative cash balance, the company said in a regulatory filing. The staggering withdrawals unfolded at a speed enabled by digital banking and were likely fueled in part by viral panic spreading on social media platforms and, reportedly, in private chat groups.

Signature Bank was also hit by a withdrawal tsunami, and right now many other regional banks are also seeing huge outflows.

- Buy All-American!

- Bring health and vitality back to your body with these non-transdermal patches

- Get your Vitamin B17 & Get 10% Off With Promo Code TIM

- How To Protect Yourself From 5G, EMF & RF Radiation - Use promo code TIM to save $$$

- The Very Best All-American Made Supplements On The Market

- Grab This Bucket Of Heirloom Seeds & Save with Promo Code TIM

- Here’s A Way You Can Stockpile Food For The Future

- Stockpile Your Ammo & Save $15 On Your First Order

- Preparing Also Means Detoxifying – Here’s One Simple Way To Detoxify

- The Very Best Chlorine Dioxide

- All-American, US Prime, High Choice Grass-Fed Beef with NO mRNA, hormones or antibiotics... ever!

So which banks will be the next to implode?

Well, on Tuesday Moody’s Investors Service suddenly slashed its outlook for the entire U.S. banking sector…

In a harsh blow to an already-reeling sector, Moody’s Investors Service cut its view on the entire banking system to negative from stable.

The firm, part of the big three rating services, said Monday it was making the move in light of key bank failures that prompted regulators to step in Sunday with a dramatic rescue plan for depositors and other institutions impacted by the crisis.

But what was far more troubling was the fact that Moody’s identified six specific banks for potential downgrades…

Moody’s also warned it was reviewing the rates of First Republic Bank, Zions, Western Alliance, Comerica, UMB Financial, and Intrust Financial. It said it had cut the rating on Signature Bank, which was seized by bank regulators over the weekend, to junk.

Needless to say, we will want to keep a very close eye on those six names.

Meanwhile, one of the most important banks in Europe has acknowledged “material weaknesses”…

Credit Suisse has acknowledged ‘material weaknesses’ in its internal controls as the Swiss bank released its annual report on Tuesday, in the latest blow to the scandal-hit bank.

The annual report was delayed following queries from U.S. regulators regarding its books. The bank was supposed to publish its report last week but it postponed the release after a last-minute call from the U.S. Securities and Exchange Commission over revisions made to cash-flow statements for 2019 and 2020.

Shares of the bank just fell to an all-time low.

Overall, Credit Suisse is now down a staggering 97 percent since 2007.

But we have known that Credit Suisse has been in trouble for years.

Sometimes these things just take time to fully play out. For example, insiders knew that Silicon Valley Bank was “technically insolvent for months” before it finally collapsed…

In fact, Silicon Valley Bank has been technically insolvent for months: the company had more assets than liabilities, but a huge chunk of those assets could not be liquidated without taking a major loss; everything would be ok, though, because those securities would mature in time, paying back their value in full. The big loser would be Silicon Valley Bank stock holders, who would forego all of the unrealized interest on the more attractive securities the bank could not buy in the meantime; small wonder the stock lost 66% of its value last year:

Many other banks that are “technically insolvent” right now may be able to survive for a while, but their days are numbered.

We are watching a slow-motion train wreck play out right in front of our eyes, and our leaders are not going to be able to stop it.

But they could at least try to make good decisions.

It turns out that there were private buyers for Silicon Valley Bank that had emerged, and having a private buyer purchase the bank would have solved a lot of problems.

Unfortunately, it is being reported that the Biden administration rejected those buyers, and if that is true than this is definitely “another Biden scandal”…

Kevin Hassett, former Chairman of the Council of Economic Advisers under Trump, told Fox Business that “there were buyers who were willing to step in & buy [SVB, but] the radicals at the @FDICgov basically weren’t going to allow that to happen … the Biden Admin had a whitelist of companies that were allowed to buy the failed bank & companies that weren’t.”

“If this is true,” said Grabien founder Tom Elliott, “then this is another Biden scandal.“

Hopefully the truth will come out about this, because if the Biden administration purposely made this crisis worse for political purposes that should make all of us deeply angry.

We have a major crisis on our hands, and now is not a time to be playing politics.

All over the nation, economic activity is slowing down and large corporations are laying off workers.

In fact, Facebook just announced a second round of layoffs…

Another 10,000 employees of Meta, the parent company of Facebook and Instagram, will be laid off, after the tech giant announced further cuts on Tuesday.

Meta CEO Mark Zuckerberg in a message to employees said he “made the difficult decision” to make the cuts, adding that recruiting employees were expected to be impacted by the layoffs this week.

We haven’t seen anything like this since 2008.

Through the end of February, announced job cuts in the United States were running 427 percent higher than they were at the same time last year.

A major economic meltdown is here, and eventually things will get a whole lot worse than they are right now.

So I would encourage you to brace yourselves for the incredibly challenging times that are ahead of us, because they will truly shake our society to the core.

Article posted with permission from Michael Snyder

{kind=link}